IRENA’s Renewable Power Generation Costs in 2025 report shows that renewable energy continues to expand its economic advantage over fossil fuels. At the same time, it highlights a paradigm shift: storage, power infrastructure, financing and energy security are now moving to the center of the sector’s strategic decisions.

Over the past decade, the energy transition has been driven by a combination of factors that has profoundly transformed the global power sector. The rapid expansion of installed capacity, industrial economies of scale and technological advances have consistently reduced the costs of solar power and wind generation, making these technologies competitive in virtually every market.

This cost reduction has been decisive in accelerating investment and increasing the share of renewable sources in the global electricity mix. However, the findings presented by the International Renewable Energy Agency (IRENA) in its Renewable Power Generation Costs in 2025 report show that the sector has entered a new stage. The discussion is no longer focused solely on producing cheaper electricity, but on building energy systems capable of combining economic competitiveness, operational resilience and energy security.

This shift does not mean that costs are no longer important. Quite the opposite. The report confirms that renewable energy remains, in most cases, the most cost-effective option for new power generation projects. What has changed is the context in which this competitiveness is now being assessed.

In a scenario marked by geopolitical tensions, rapidly growing electricity demand, the electrification of new sectors of the economy and the need to modernize power grids, factors such as energy storage, operational flexibility and access to financing are now directly influencing the pace of the energy transition.

Renewables remain the most competitive option

The figures presented by IRENA reinforce a trend that has been consolidating in recent years. In 2025, more than 90% of the utility-scale renewable capacity added globally generated electricity at costs lower than the cheapest fossil fuel alternative available in each market.

This competitiveness is the result of a consistent cost reduction trajectory over the past fifteen years.

Since 2010:

- the levelized cost of electricity (LCOE) of solar photovoltaic fell by 89%;

- concentrated solar power (CSP) reduced its cost by 72%;

- onshore wind generation recorded a 71% reduction;

- offshore wind generation registered a 63% decline.

In 2025, the global weighted average LCOE remained at USD 44/MWh for solar photovoltaic, USD 33/MWh for onshore wind and USD 78/MWh for offshore wind, values that keep these technologies among the most competitive options for expanding power generation.

These results show that the economic advantage of renewables is no longer a projection, but a consolidated reality across a large share of global markets.

Competitiveness now also means economic protection

One of the most relevant aspects of the report is that it broadens the discussion around the economic value of renewable energy.

Because they do not depend on the continuous purchase of fuels to operate, renewable power plants reduce the exposure of consumers, companies and governments to volatility in international oil, natural gas and coal markets.

According to IRENA, existing renewable generation avoided approximately USD 480 billion in fossil fuel costs in 2025, while also avoiding around 8.4 gigatonnes of carbon dioxide emissions.

The report highlights that these savings have a particular behavior: their value increases precisely during periods of rising international fossil fuel prices, functioning as an important mechanism of economic protection.

This characteristic became evident during the crisis caused by the closure of the Strait of Hormuz in early 2026. The rise in oil and gas prices significantly increased energy import costs in several countries. In contrast, power systems with a higher share of renewables reduced their exposure to fluctuations in the international fuel market.

The study uses Indonesia, Thailand and the Philippines as examples. In these three economies, existing renewable generation avoided approximately USD 5.7 billion in coal and gas purchases based on average 2025 prices. When recalculated using the prices observed during the crisis between March and May 2026, this economic benefit rises to USD 6.5 billion. If renewable generation in these countries had been twice the level recorded in 2025, the savings would have reached approximately USD 12.9 billion.

These results reinforce an important message from the report: in addition to reducing emissions, renewable energy contributes to strengthening the economic resilience of countries that depend on fossil fuel imports.

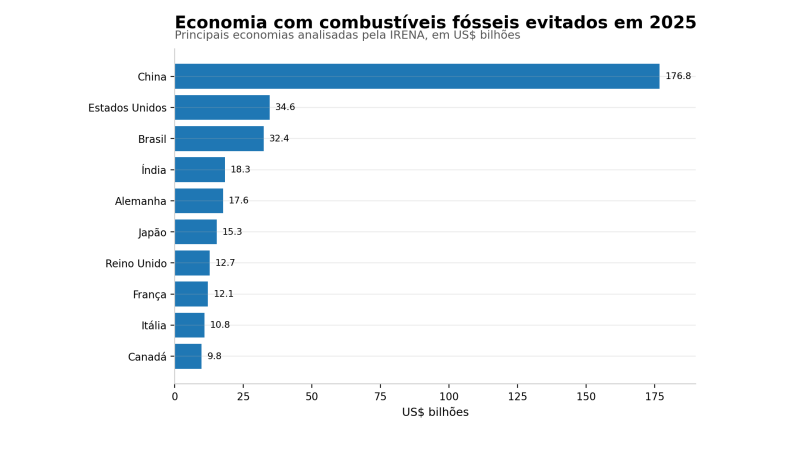

Brazil is among the main beneficiaries

The report also presents a comparison of the countries that most reduced fossil fuel spending thanks to renewable generation.

Brazil ranks third, with estimated savings of USD 32.4 billion in 2025, behind only China and the United States.

IRENA itself makes an important methodological observation about this result. Brazil’s strong performance does not necessarily stem from the recent replacement of large volumes of fossil fuel generation, but from the historically high share of hydropower in the country’s electricity mix. In other words, the calculation considers the volume of fossil fuels that would have been required if this renewable generation had not been available.

Even so, the result highlights an important characteristic of Brazil’s power mix: the high share of renewable sources helps reduce operating costs and lower exposure to international fuel price fluctuations.

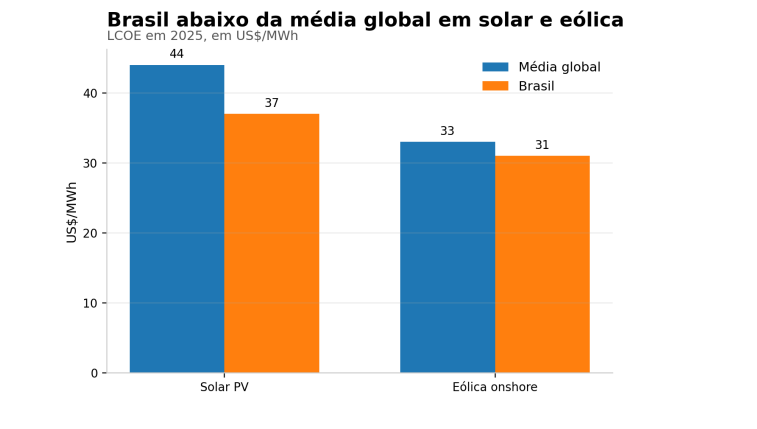

Another figure that reinforces this competitiveness appears in the comparison of average generation costs.

In 2025, the levelized cost of solar photovoltaic power in Brazil was estimated at USD 37/MWh, below the global average of USD 44/MWh. For onshore wind generation, Brazil’s cost reached USD 31/MWh, also below the global average of USD 33/MWh.

These indicators place the country among the most competitive markets for the expansion of these technologies, although the report itself emphasizes that future competitiveness will increasingly depend on power infrastructure, access to financing and regulatory stability.

Storage is no longer a complement and is becoming part of new projects

If cost reduction marked the first phase of the energy transition, the integration of renewable generation and storage is emerging as one of the main features of this new stage.

The report shows that approximately 25% of all new utility-scale solar capacity installed in 2025 was paired with battery storage systems. In locations with high-quality solar resources, the levelized cost of electricity (LCOE) of these hybrid systems was below USD 85/MWh, demonstrating that the combination of generation and storage is becoming economically viable in several markets.

This movement responds to a practical need within the power system.

As the share of variable sources, such as solar and wind, increases, so does the importance of technologies capable of providing operational flexibility, reducing fluctuations in energy supply and improving the use of existing infrastructure.

The report indicates that the costs of these hybrid systems are expected to continue falling in the coming years, although at a more moderate pace than that observed over the past decade. While consolidated technologies, such as solar photovoltaic and onshore wind, are entering a phase of cost stabilization, batteries and long-duration storage solutions are expected to continue advancing as their deployment increases.

Another relevant figure concerns the cost of batteries themselves.

According to IRENA, the price of utility-scale storage systems fell by approximately 30% in 2025, reaching around USD 140/kWh. Compared with 2010, the accumulated reduction is close to 95%, as a result of expanded production capacity, technological progress and greater manufacturing scale.

These figures indicate that storage is moving beyond a niche solution and is beginning to play a structural role in the expansion of power systems.

The next decade will be marked by technological maturity

Although the competitiveness of renewable energy continues to increase, the report suggests that the sector is entering a different phase from the one observed between 2010 and 2025.

During that period, the main driver of cost reduction was the rapid expansion of manufacturing, especially in China, accompanied by significant productivity gains, industrial innovation and economies of scale.

Now, several indicators point to a stabilization of this process.

Global investment in the manufacturing of clean technologies fell by approximately 50% compared with the peak recorded in 2023. According to IRENA, this reduction is mainly associated with China’s efforts to contain excess production capacity in the solar sector and with recent changes in United States industrial policy.

This new dynamic may influence global supply chains, component prices and the pace of expansion of production capacity.

At the same time, the report highlights that external factors, such as fluctuations in the price of metals used in batteries, continue to influence the costs of emerging technologies.

The increase observed in the price of these inputs in early 2026 demonstrates that future cost reductions may occur in a less linear way than over the past decade.

This shift does not represent a loss of competitiveness for renewable energy.

It indicates that the sector is entering a more mature phase, in which operational efficiency, incremental innovation and supply chain stability are becoming as influential as direct reductions in technology costs.

Financing is becoming as important as technology

Among the report’s most relevant conclusions is a change in perspective regarding the factors that determine the competitiveness of new projects.

According to IRENA, where a project is developed now has a greater influence on the final cost of generation than the technology used.

The analysis shows that national macroeconomic conditions explain approximately 2.3 times more of the variation in financing costs than technological differences between projects.

In practice, this means that factors such as regulatory stability, country risk, access to credit and the cost of capital are becoming decisive for the pace of renewable energy expansion.

Even highly competitive technologies can present high costs when developed in environments with a greater perception of financial risk.

This finding expands the role of public policies.

In addition to encouraging technological innovation, countries are now competing in their ability to offer legal certainty, regulatory predictability and adequate financing conditions for new investments.

Emerging technologies expand the possibilities of the transition

Although solar photovoltaic and wind continue to concentrate most investments, the report also devotes attention to technologies that may gain ground over the next decade.

These include sodium-ion batteries, whose economic potential increases as lithium prices rise, as well as perovskite solar cells, which are approaching the commercial stage. The study also highlights favorable prospects for long-duration storage solutions, such as flow batteries and compressed air systems, as well as for ocean technologies, including wave and tidal energy.

Although many of these solutions are still in the process of consolidation, the trend observed by IRENA is a gradual expansion of the technological portfolio available to support the decarbonization of power systems.

This progress should help increase operational flexibility and reduce dependence on a single technology, strengthening energy security across different regional contexts.

Brazil has competitive advantages, but the next challenge will be structural

The indicators presented by IRENA show that Brazil holds a distinctive position in the international landscape. In addition to having an electricity mix with a high share of renewable sources, the country maintains solar photovoltaic and wind generation costs below global averages, as a result of the combination of natural resource availability, technological maturity and favorable conditions for project deployment.

However, the report itself shows that this advantage alone will not be enough to sustain leadership over the next decade.

As the share of renewable sources increases, investment is no longer concentrated only on building new solar and wind farms. Expansion now depends on a broader set of factors, including power grids, storage, digitalization, system-wide planning and adequate financing conditions.

This change alters the nature of competitiveness between countries.

Until a few years ago, the main question was where to produce renewable energy at the lowest possible cost. Now, it is equally important to identify which markets can integrate large volumes of variable generation with efficiency, reliability and operational stability.

In this context, Brazil has favorable characteristics.

The high share of hydropower provides a regulation capacity that few power systems possess. The expansion of solar and wind generation increases the diversification of the electricity mix, while the advancement of storage creates new possibilities to increase power system flexibility.

The report does not establish specific projections for Brazil nor does it analyze the country’s energy policy. Even so, its findings reinforce that countries capable of combining competitive renewable generation with adequate infrastructure tend to expand their economic advantage in the coming years.

The competitiveness of renewables has entered a new stage

Perhaps the main contribution of the Renewable Power Generation Costs in 2025 report is not confirming that solar and wind remain cheaper.

This conclusion has already been demonstrated by IRENA itself for several years.

The distinguishing feature of this edition is that it shows that generation cost is no longer the only relevant indicator for assessing the competitiveness of renewable energy.

The results presented show that factors such as storage, power infrastructure, financing, regulatory stability, supply chains and economic resilience are exerting growing influence over the pace of the energy transition.

This perception also changes the way governments, investors and companies evaluate new projects.

The expansion of renewables remains essential for reducing greenhouse gas emissions. However, its benefits are now also being observed from the perspective of energy security, reduced exposure to fluctuations in international fuel markets and economic competitiveness.

In an international scenario marked by greater geopolitical volatility, this characteristic gains additional importance.

The report shows that power systems with a higher share of renewable sources are less sensitive to variations in fossil fuel prices, functioning as an important mechanism of economic protection.

More than producing clean electricity, these systems now provide cost predictability, greater stability for consumers and companies, and less dependence on external factors.

Conclusion

Over the past decade, the energy transition was driven primarily by the reduction in the cost of renewable technologies.

The figures presented by IRENA show that this stage was successful.

Solar photovoltaic, wind generation and other renewable sources have consolidated themselves as competitive alternatives for new projects across virtually every continent. More than 90% of the renewable capacity added in 2025 generated electricity at costs lower than the cheapest fossil fuel alternative available.

At the same time, existing renewable generation avoided approximately USD 480 billion in fossil fuel costs and around 8.4 gigatonnes of carbon dioxide emissions in 2025 alone, demonstrating that its benefits go beyond the environmental dimension.

These results indicate that the energy transition is entering a new phase.

The challenge is no longer only to expand installed renewable generation capacity. It now involves building more resilient power systems, capable of integrating storage, increasing operational flexibility, strengthening transmission and distribution grids, and creating the conditions for new investments to take place sustainably.

For countries such as Brazil, which already have a predominantly renewable electricity mix and competitive generation costs, this new stage represents an opportunity to consolidate structural advantages and increase their relevance in the global transformation of the power sector.

More than producing low-carbon energy, the next decade will be marked by the ability to turn this energy into a strategic asset for competitiveness, energy security and economic development.

{kind=link}

Comment